The government’s ambition of making India a global manufacturing hub has led to an increased focus on the core and emerging sectors by promoting ease of doing business and measures to upgrade public works and boost digitization.

Finance Minister Nirmala Sitharaman is expected to reaffirm the government’s commitment to boosting growth by focusing on infrastructure creation and manufacturing in the budget for FY 2024 she will present on February 1.

But road-related capital expenditure may stay flat, experts say, citing concerns over the growing debt of the National Highways Authority of India (NHAI).

Last year saw earnings upgrades and robust order flows for most industrial companies, wrote financial services firm Jefferies in a note to clients. Although order flow growth may slow in 2023, operating leverage should continue to surprise, it added.

“Power T&D (Transmission and Distribution), Railways, Data Centres, Logistics, PLI (Production-Linked Incentive schemes) and Metals are the sub-segments we are more positive on,” Jefferies wrote.

“Budget 2024 commentary dropping capex focus is a potential red flag,” the firm wrote.

Market participants have pointed out that the budgetary allocation for infrastructure capex has gone up substantially over the past few years.

The government’s ambition of making India a global manufacturing hub has led to an increased focus on the core and emerging sectors by promoting ease of doing business and measures to upgrade public works and boost digitization.

The government is also looking at the Nation Asset Monetisation Plan to support the ambitious targets set under the National Infrastructure Pipeline.

Market participants say the government will continue to focus on infrastructure development, broad-based capital expenditure and manufacturing-led growth.

“The FY2024 Union Budget should remain focused on pro-growth initiatives such as continued infrastructure and capacity development investment,” said Manish Goel, founder & director, Research and Ranking.

Jefferies noted that the FY24 budget is the last material one before the national elections due in May 2024. The February 2024 budget cannot make material changes because of election embargo rules.

Nomura explained that the government’s focus is usually on electorally popular measures ahead of polls, the reason why it expects awards for road construction to not pick up in FY24. It has noted the trend of a slowdown in road-building orders ahead of the general elections in FY09, FY14 and FY19. A key reason is that the Election Commission of India enforces a Model Code of Conduct just ahead of the elections.

The government’s infra push has increased demand for construction material and equipment.

HDFC Securities believes that in the long term, India may emerge as an alternative manufacturing hub for global markets. It said multinationals were expanding capacity in India to cater to domestic as well as global demand. The share of exports in the order book and revenue is also increasing.

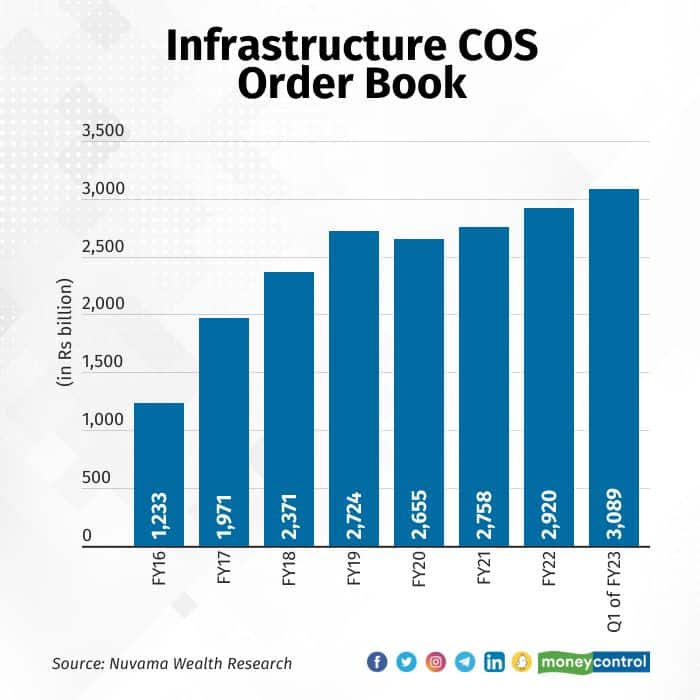

Excluding Larsen & Toubro (L&T), the order books at infra companies are at multi-year highs and have broken out of range of Rs 2.7-2.9 trillion seen over the past four years, data collected by Nuvama Wealth Research showed.

So far in FY23, valuation comfort, robust balance sheets, and strong order inflows have helped stock-specific rerating.

With inflation concerns easing, commodity prices cooling, and interest rate tightening set to ease, HDFC Securities expects further stock-specific rerating to play out.

The Nifty Infra index in the past one year is up 2 percent, but has risen nearly 7 percent in the past six months.

On road construction specifically, Kotak Institutional Equities said the financial results for the third quarter of FY23 will reflect improved execution on the fairly strong order books of road companies.

Even so, capex on the road sector is tipped to remain flat in the upcoming Budget, mainly because of the mounting debt of NHAI, which develops, maintains and manages the National Highways entrusted to it by the Centre by awarding road contracts.

The debt of NHAI increased to Rs 3.5 trillion in FY22 from around Rs 242 billion in FY15.

Nomura highlighted in a report dated December 10, 2022, that the macro situation for roads and highways is likely to deteriorate over FY24 and budget allocation will strain the ordering activity.

“Weak Budget allocation in FY23BE (Budget Estimate) (effective increase of 1% y-y) does not promise a turnaround in FY23F; with general elections due in May-24, we do not expect a turnaround in ordering for FY24,” wrote Priyankar Biswas and Neelotpal Sahu of Nomura in the report.

IIFL Securities pointed out that ordering for National Highways has been relatively slow with 5,007 km awarded until October 2022, up 2 percent Year-on-Year (YoY).

Even so, several market participants are upbeat about companies such as IRB Infrastructure Developers, PNC Infratech and KNR Constructions.

IIFL Securities wrote: “Allocation in the upcoming budget would be keenly watched and would be a key trigger for re-rating”. Its top picks include PNC Infratech, HG Infra and KNR Constructions, among highway developers, and Powermech Projects among general contractors.

Experts are keeping a close watch on the road monetisation scheme and any announcement on that front would be crucial.